Global Trends Driving Policy Shifts

The global landscape of energy production and consumption is undergoing a profound transformation, driven by an intricate web of macroeconomic and geopolitical forces. These dynamics are significantly influencing current and upcoming Renewable Energy Trade Policy Shifts worldwide, reshaping how nations interact, invest, and innovate in the clean energy sector. Understanding these overarching trends is crucial for businesses and policymakers navigating the complex future of global trade in renewable technologies and resources.

1. Geopolitical Tensions & Energy Security

Recent global events, most notably the conflict in Eastern Europe, have starkly underscored the vulnerabilities inherent in an over-reliance on centralized fossil fuel supplies. This has propelled energy security to the forefront of national policy agendas, accelerating the global pivot towards indigenous and diversified renewable energy sources. Nations are increasingly viewing renewable energy not just as an environmental imperative but as a strategic asset for bolstering national sovereignty and reducing external dependencies. This shift is driving a global push for renewable energy supply chain resilience, with governments actively seeking to diversify their sourcing for critical materials and components, reducing reliance on single geographic regions. This often manifests in policies promoting domestic manufacturing, strategic alliances, and even reshoring initiatives. Consequently, we are witnessing a surge in bilateral and multilateral agreements aimed at securing supply routes and fostering reciprocal investments in renewable energy infrastructure. The increased scrutiny over sourcing practices and manufacturing locations also directly impacts Global solar panel trade regulations, leading to a complex web of anti-dumping duties, subsidies, and import restrictions, all designed to balance free trade with national security and ethical production concerns. The geopolitical chessboard is thus directly influencing the flow of renewable energy goods and services, transforming what was once primarily an economic discussion into a strategic security imperative.

2. Economic Imperatives for Green Growth

Beyond security concerns, a powerful economic rationale is propelling Renewable Energy Trade Policy Shifts. Governments worldwide recognize the immense potential of the green economy to stimulate growth, create jobs, and foster innovation. Investments in renewables are increasingly seen as a pathway to industrial competitiveness and future prosperity. This perspective has led to significant green stimulus packages and industrial policies designed to accelerate the adoption and production of renewable technologies. Nations are vying to become leaders in emerging green industries, such as the production and trade of green hydrogen. Green hydrogen trade policies are rapidly evolving, with countries establishing bilateral agreements and developing infrastructure to facilitate its production, transport, and export. This creates entirely new economic corridors and trade relationships, potentially reshaping global energy markets. The falling costs of solar, wind, and battery storage technologies, coupled with government incentives, make renewables not only environmentally sound but also economically attractive. This competitive landscape drives continuous innovation and further cost reductions, enhancing the global trade in these technologies. Countries are also keen to secure market access for their green technologies and services, leading to negotiations around intellectual property rights and standardization in global trade agreements. The pursuit of sustainable economic development is thus a key catalyst for these policy shifts, fostering a race to the top in green industrial capabilities.

3. Evolving Climate Targets & Commitments

The urgent and undeniable reality of climate change continues to be a primary driver for Renewable Energy Trade Policy Shifts. As the scientific consensus strengthens and the impacts of global warming become more apparent, nations are under increasing pressure to set and meet more ambitious climate targets. The Paris Agreement’s framework, with its Nationally Determined Contributions (NDCs), serves as a constant impetus for countries to decarbonize their economies. This commitment translates directly into policies that favor renewable energy adoption and discourage fossil fuel use, often through market mechanisms and regulatory frameworks that impact international trade. A prominent example is the EU carbon border adjustment mechanism renewable energy (CBAM). This mechanism aims to prevent ‘carbon leakage’ by imposing a carbon levy on imports from countries with less stringent climate policies. While complex, CBAM is designed to incentivize global partners to decarbonize their industrial production, thereby indirectly promoting the trade in lower-carbon goods and renewable energy components. Such policies, alongside carbon pricing schemes and emission reduction targets, create a global market demand for sustainable products and cleaner production methods. International collaboration on climate goals also encourages technology transfer and capacity building in developing nations, further influencing trade flows in renewable energy solutions. The global commitment to a net-zero future is therefore not just an environmental aspiration but a powerful economic and regulatory force fundamentally altering the landscape of international trade in the renewable energy sector.

Fortifying Renewable Supply Chain Resilience

The global energy landscape is undergoing a profound transformation, with Renewable Energy Trade Policy Shifts at its forefront. However, this transition is not without its challenges, particularly concerning the resilience of its supply chains. Amidst increasing geopolitical tensions, natural disasters, and the lingering effects of global pandemics, the vulnerabilities within the renewable energy supply chain have become starkly apparent. Dependencies on single-source suppliers for critical components, raw materials, and manufacturing capabilities pose significant risks to the pace and security of the clean energy transition. In response, governments worldwide are implementing new policies designed to secure and diversify these vital networks, aiming to build robust renewable energy supply chain resilience and mitigate future disruptions. These proactive measures encompass a range of strategies, from fostering domestic production to forging international alliances, all geared towards a more stable and sustainable energy future.

1. Local Content Requirements & Incentives

One of the primary strategies to strengthen the renewable energy supply chain involves the implementation of local content requirements (LCRs) and various incentives. Local content requirements mandate that a certain percentage of components, services, or labor for renewable energy projects must be sourced domestically. This policy aims to stimulate local manufacturing, assembly, and service industries, thereby reducing reliance on foreign imports and fostering job creation within the country. For example, some Global solar panel trade regulations are increasingly incorporating such provisions. Alongside LCRs, governments are offering a suite of incentives to encourage domestic investment in renewable energy manufacturing. These can include tax credits, direct subsidies, preferential procurement policies, and low-interest loans for companies that establish or expand their production facilities locally. The objective is not only to boost local economies but also to create a diversified manufacturing base, ensuring that essential components—from wind turbine blades to battery storage systems—are readily available from multiple sources, lessening the impact of disruptions elsewhere.

2. Critical Minerals Sourcing & Strategic Alliances

The transition to clean energy is heavily reliant on critical minerals such as lithium, cobalt, nickel, and rare earth elements, which are essential for technologies like electric vehicles, wind turbines, and solar panels. The concentration of mining and processing of these minerals in a few countries presents a significant supply chain vulnerability. To address this, policies are focusing on diversifying critical minerals sourcing through several avenues. This includes investing in domestic exploration and extraction where feasible, promoting advanced recycling technologies to recover valuable materials from end-of-life products, and establishing strategic alliances with resource-rich nations. These alliances often involve long-term supply agreements, joint ventures in mining and processing, and technical cooperation to develop sustainable extraction methods. Furthermore, new Green hydrogen trade policies are also exploring how to secure necessary catalysts and components for electrolysis, often tied to critical mineral availability. Such diplomatic and economic partnerships are crucial for creating a more secure and predictable supply of these indispensable materials, underpinning the expansion of renewable energy infrastructure globally.

3. De-risking Manufacturing & Distribution Networks

Beyond local production and raw material sourcing, policies are also targeting the broader de-risking of manufacturing and distribution networks. This involves strategies to enhance the overall resilience of the supply chain, making it less susceptible to localized shocks. One key approach is geographical diversification of manufacturing facilities, encouraging companies to establish production sites in multiple regions rather than concentrating them in a single location. This reduces the impact of disruptions like pandemics, natural disasters, or trade disputes in any one area. Investment in advanced manufacturing technologies, such as automation and digital twin simulations, can also enhance efficiency and adaptability. Furthermore, policies are promoting improved logistics and transportation networks, including diversified shipping routes and increased port capacities, to ensure the smooth flow of components. The EU carbon border adjustment mechanism renewable energy (CBAM), for instance, aims to level the playing field for industries with high carbon footprints, subtly influencing manufacturing locations and encouraging greener production, which can contribute to a more resilient, localized, and environmentally responsible supply chain. By fostering greater transparency and traceability throughout the distribution network, these measures aim to create a dynamic and adaptable supply chain capable of withstanding future shocks and supporting the continuous growth of renewable energy.

Navigating Global Solar Panel Trade Regulations

A deep dive into the latest international regulations, tariffs, and non-tariff barriers affecting the global trade of solar panels and components.

The global solar energy industry is at a pivotal juncture, grappling with a complex web of international trade regulations that significantly influence Renewable Energy Trade Policy Shifts. As nations accelerate their transition to green economies, the demand for solar panels and components continues to surge. However, this growth is increasingly complicated by protectionist measures, evolving customs duties, and strategic geopolitical maneuvers aimed at shaping renewable energy supply chain resilience. Understanding these dynamics is crucial for manufacturers, suppliers, and investors looking to navigate the intricate landscape of global solar panel trade regulations.

1. Anti-Dumping & Countervailing Duty Updates

Anti-Dumping (AD) and Countervailing Duties (CVD) are trade remedies imposed by importing countries to counteract unfair trade practices. Anti-dumping duties address situations where foreign producers sell goods in an export market at prices below their domestic market value or production cost, harming the domestic industry. Countervailing duties, on the other hand, target goods whose production has been subsidized by the exporting country’s government, giving them an unfair competitive advantage. The solar panel sector has historically been a frequent target of such measures, particularly concerning products originating from major manufacturing hubs.

Recent years have seen a surge in AD/CVD investigations and impositions, especially by the United States and the European Union against solar products from Southeast Asia and China. These updates directly impact the cost of imported solar panels, often leading to price volatility and shifts in procurement strategies. Businesses must continuously monitor these trade actions, as they can redefine market competitiveness and significantly alter the profitability of international solar trade. For more comprehensive information on these trade remedies, consult the World Trade Organization’s (WTO) overview of Anti-Dumping agreements.

2. Regional Protectionism vs. Free Trade Agendas

A growing tension exists between regional protectionist policies designed to foster domestic manufacturing and the broader principles of free trade that advocate for open markets and global competition. Many governments are implementing incentives and local content requirements to bolster their internal solar industries, citing national security, job creation, and the desire for renewable energy supply chain resilience. Examples include the U.S. Inflation Reduction Act’s domestic manufacturing credits and the EU’s Net-Zero Industry Act proposals.

While these initiatives aim to de-risk supply chains and promote local economic growth, they often introduce non-tariff barriers, complicate international sourcing, and can lead to fragmentation of the global market. The long-term implications for global solar panel trade regulations are substantial, potentially leading to higher costs for consumers and slower deployment rates in regions reliant on imports. Balancing these protectionist urges with the economic efficiencies offered by free trade remains a critical challenge for policymakers worldwide, especially as discussions around green hydrogen trade policies also begin to intensify.

3. Impact on Production Costs & Market Access

The myriad of global solar panel trade regulations, including tariffs, AD/CVD duties, and local content requirements, directly escalates production costs and restricts market access for solar manufacturers. Tariffs add a direct cost to imported components and finished products, which is often passed on to consumers. Furthermore, complying with diverse regulatory frameworks, such as navigating complex customs procedures or adhering to specific sustainability standards, incurs additional operational expenses.

For instance, the impending EU Carbon Border Adjustment Mechanism (CBAM) renewable energy provisions, while not directly targeting solar panels yet, signal a future where carbon intensity could become a critical trade barrier. Manufacturers will need to invest in cleaner production methods to maintain competitiveness in certain markets. These regulations compel companies to rethink their global manufacturing and sourcing strategies, often leading to investments in diversified production facilities in multiple countries to mitigate risks and ensure continued market access. Ultimately, the ability to adapt to these shifting policies will determine which players thrive in the evolving global solar landscape.

Green Hydrogen: Emerging Trade Policies & Standards

The global energy landscape is undergoing a profound transformation, with green hydrogen emerging as a pivotal player in the transition towards decarbonization. Produced by electrolyzing water using renewable electricity, green hydrogen offers a versatile, clean energy carrier with the potential to decarbonize hard-to-abate sectors like heavy industry, long-haul transport, and aviation. However, unlocking its full international trade potential requires navigating a complex and evolving landscape of Renewable Energy Trade Policy Shifts. This nascent market is characterized by rapidly evolving trade policies, intricate certification schemes, and ambitious infrastructure developments, all critical for establishing a robust global green hydrogen economy and ensuring renewable energy supply chain resilience.

1. Cross-Border Infrastructure Development

The vision of a global green hydrogen market hinges on the development of extensive and efficient cross-border infrastructure. Unlike traditional fossil fuels, green hydrogen, or its derivatives like ammonia or liquid organic hydrogen carriers (LOHCs), requires specialized transportation and storage solutions. Current initiatives include repurposing existing natural gas pipelines for hydrogen blending or dedicated hydrogen transport, as well as constructing new pipelines across continents. For intercontinental trade, investments in new port terminals capable of handling liquefied hydrogen or ammonia carriers are paramount. Major projects are already underway, such as the European Hydrogen Backbone initiative, aiming to connect hydrogen supply and demand centers across Europe through a network of pipelines. Similarly, strategic alliances are forming between nations in the Asia-Pacific region to facilitate maritime trade routes for hydrogen derivatives. Challenges include the significant capital investment required, differing technical standards across borders, and the need for multilateral agreements to streamline regulatory approvals. The success of these infrastructure endeavors is crucial not only for green hydrogen trade policies but also for reinforcing the broader global renewable energy supply chain resilience, ensuring that regions with abundant renewable resources can effectively supply energy to demand centers worldwide. This complex web of infrastructure development also subtly impacts considerations related to global solar panel trade regulations, as the very inputs for green hydrogen production (renewable electricity) rely heavily on solar and wind technologies whose supply chains are subject to international trade dynamics.

2. Certification & Origin Guarantees

Ensuring the environmental integrity of “green” hydrogen is fundamental to its market acceptance and trade. This necessitates robust certification schemes and origin guarantees that verifiably track hydrogen production from its renewable energy source to its point of consumption. Without clear, internationally recognized standards, the risk of greenwashing and market fragmentation is high. Various approaches are being explored, including direct physical tracking, mass balance systems (where green attributes are matched to consumption within a defined system), and book & claim mechanisms (where attributes are unbundled and traded separately). Key players like the EU, Japan, and Germany are developing their own national and regional certification frameworks, often specifying criteria for lifecycle greenhouse gas emissions, renewable energy input sources, and water usage. The EU’s Renewable Energy Directive (RED II and upcoming RED III) provides a framework for defining renewable fuels of non-biological origin (RFNBOs), crucial for hydrogen. Harmonization of these diverse standards is a top priority for facilitating international green hydrogen trade policies. The development of a global certification framework, perhaps under the auspices of an international body, would simplify cross-border transactions and instill greater confidence among buyers and investors. Furthermore, the interplay between green hydrogen imports and mechanisms such as the EU carbon border adjustment mechanism renewable energy is increasingly relevant, as imported hydrogen’s carbon intensity will likely factor into future carbon pricing and trade tariffs.

3. Subsidies & Incentives for Production & Export

The nascent stage of the green hydrogen industry means that production costs are currently higher than conventional, fossil-fuel-derived hydrogen. Consequently, government subsidies and incentives play a critical role in bridging this cost gap, stimulating investment, and scaling up production capacity. These measures vary widely across countries, ranging from direct production tax credits (e.g., the U.S. Inflation Reduction Act’s 45V credit), investment grants, and loan guarantees, to carbon contracts for difference (CCfDs) that guarantee a minimum carbon price for green products. Some nations are also exploring export-focused incentives to position themselves as future hydrogen exporters. While essential for kickstarting the market, these subsidies also introduce complexities into international trade. Concerns about potential trade distortions, unfair competition, and the emergence of “subsidy races” are beginning to surface. The World Trade Organization (WTO) framework, designed for traditional goods and services, may need re-evaluation or adaptation to effectively address these new dynamics in energy trade. Developing a balanced approach that supports industry growth without unduly impacting fair trade practices is a a significant policy challenge. These Green hydrogen trade policies and incentive structures are crucial elements of the broader Renewable Energy Trade Policy Shifts, shaping the competitive landscape and accelerating the global adoption of this vital clean energy vector.

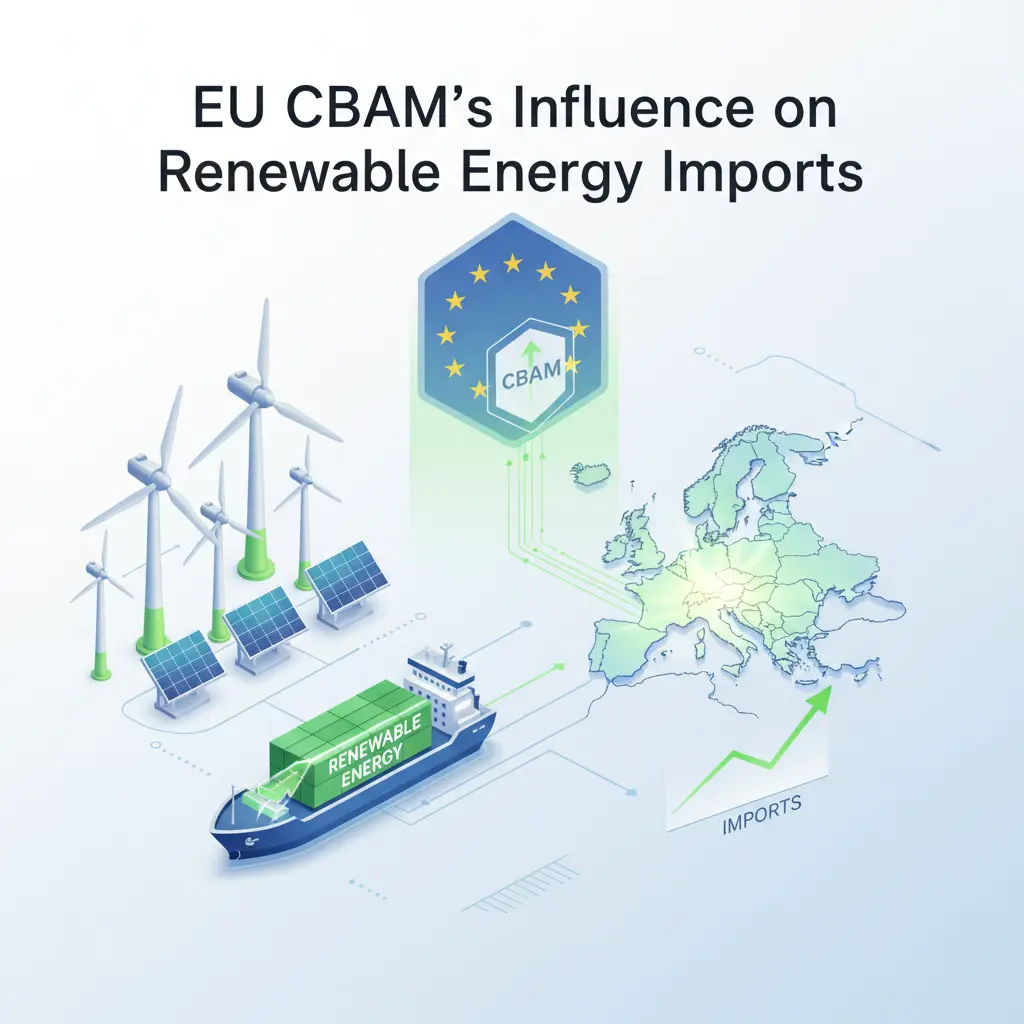

EU CBAM’s Influence on Renewable Energy Imports

The European Union’s Carbon Border Adjustment Mechanism (CBAM) represents a landmark shift in global trade, primarily targeting carbon-intensive industries. While initial focus has been on sectors like cement, iron, steel, aluminum, fertilizers, and electricity, its indirect and direct implications for the import of renewable energy technologies and components are profound. This mechanism is poised to reshape Renewable Energy Trade Policy Shifts, compelling non-EU exporters to account for the embedded carbon emissions of their products before entering the EU market. For the rapidly expanding renewable energy sector, which relies heavily on international supply chains for components like solar panels, wind turbine parts, and materials for green hydrogen production, understanding and adapting to CBAM is crucial for maintaining competitive access to the lucrative EU market. The aim is to prevent carbon leakage, ensuring that the EU’s ambitious climate policies are not undermined by the outsourcing of carbon-intensive production to countries with less stringent environmental regulations.

1. Compliance Challenges for Exporters

Exporters of renewable energy components and technologies to the EU face significant compliance hurdles under CBAM. While finished solar panels or wind turbines themselves might be seen as ‘green’ products, the embedded emissions in their raw materials (e.g., steel, aluminum, polysilicon) and manufacturing processes will be scrutinized. This requires a granular understanding and transparent reporting of carbon emissions across the entire supply chain. Non-EU manufacturers must accurately calculate the direct and indirect greenhouse gas emissions associated with the production of their goods. This includes Scope 1 emissions (direct emissions from owned or controlled sources) and Scope 2 emissions (indirect emissions from the generation of purchased energy). The complexity arises from varying national regulations on emissions monitoring, the need for robust data collection systems, and potentially differing methodologies for carbon accounting. For many, this will necessitate significant investment in tracking software, expertise, and potentially independent verification to meet EU standards. Failure to comply could lead to financial penalties, increased administrative burden, or even market access restrictions, thus impacting the Renewable energy supply chain resilience for the EU. The transitional phase (October 2023 – December 2025) allows for learning and adaptation, but the clock is ticking for exporters to develop sophisticated carbon footprint assessment capabilities.

2. Impact on Manufacturing Footprints

CBAM is poised to exert considerable influence on the global manufacturing footprints of renewable energy component producers. Faced with potential CBAM charges, non-EU manufacturers may be incentivized to decarbonize their production processes or even relocate parts of their manufacturing to regions with lower carbon intensity or more advanced green energy grids. This could lead to a strategic reassessment of where key components, such as ingots, wafers, and cells for solar panels, or specific metals for wind turbine generators, are produced. For instance, a producer of solar cells in a coal-reliant energy grid might find their products less competitive in the EU market compared to a producer operating on a renewable energy-dominated grid, even if production costs are otherwise similar. This pressure is intended to foster a global race to the top in terms of green manufacturing practices, potentially leading to significant shifts in Global solar panel trade regulations. Conversely, some manufacturers might explore nearshoring or reshoring production within the EU or to countries with existing robust carbon pricing mechanisms that are linked to the EU ETS, effectively avoiding the CBAM levy. This strategic realignment aims not only to reduce CBAM costs but also to enhance overall supply chain sustainability and reduce geopolitical risks associated with distant manufacturing hubs. The long-term effect could be a more localized and greener manufacturing base for renewable energy components, aligning with the EU’s broader climate objectives.

3. Strategic Responses from Non-EU Nations

Non-EU nations, particularly major exporters of renewable energy components, are developing multifaceted strategic responses to CBAM. These responses range from advocating for exemptions or special provisions to actively implementing their own carbon pricing mechanisms. For countries heavily involved in the EU carbon border adjustment mechanism renewable energy supply chain, the imperative is to ensure their industries remain competitive. Some nations are exploring bilateral agreements with the EU to recognize equivalent carbon pricing schemes, which could effectively exempt their products from CBAM charges. Others are investing heavily in national decarbonization strategies, focusing on transitioning their energy grids to renewables and promoting low-carbon industrial processes. For example, countries like Vietnam, a significant exporter of solar panels, are likely to accelerate their green energy transition efforts to reduce embedded emissions in their manufactured goods destined for Europe. This proactive approach not only mitigates CBAM risks but also aligns with global climate goals and enhances the long-term sustainability of their export industries. Furthermore, some non-EU governments are providing financial incentives and technical assistance to their domestic industries to help them adapt to CBAM’s reporting requirements and decarbonize their production. The overarching goal is to transform CBAM from a trade barrier into an accelerator for global climate action, encouraging a worldwide shift towards more sustainable manufacturing and fostering international cooperation on carbon reduction efforts. More information on the European Commission’s stance can be found on their official page regarding CBAM implementation.

Partner with Vietnam’s Leading Suppliers

Looking for reliable suppliers in Vietnam? Contact VietnamSuppliers.com today to connect with verified manufacturers and exporters across all industries.

—————————————

References

– IEA Critical Minerals Market Review 2023: https://www.iea.org/reports/critical-minerals-market-review-2023

– The Role of Critical Minerals in Clean Energy Transitions – IEA: https://www.iea.org/reports/the-role-of-critical-minerals-in-clean-energy-transitions

– :

– global renewable energy supply chain resilience: https://www.iea.org/reports/global-hydrogen-review-2023

– CBAM implementation: https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en