Understanding the Red Sea Crisis: A Global Overview

The Red Sea has historically been a crucible of trade and geopolitics, but recent events have escalated its strategic importance into a critical global concern. This section provides a concise overview of the Red Sea Shipping Crisis Impact, detailing its origins, the key players involved, and the immediate geopolitical and economic triggers that have led to significant disruptions in major maritime trade routes. The ongoing crisis is reshaping global supply chain disruptions in 2024, forcing a reassessment of maritime risk assessment reports and influencing the international freight rates forecast, prompting urgent discussions on trade route diversification strategies.

Geopolitical Background of Houthi Attacks

The current crisis stems predominantly from attacks carried out by the Houthi movement (Ansar Allah), an Iran-aligned group controlling large parts of Yemen. Originating from the protracted civil war in Yemen, the Houthis have increasingly leveraged their control over strategic coastal areas to launch drone and missile attacks on commercial vessels navigating the Red Sea. These actions, which began intensifying in late 2023, are presented by the Houthis as a show of solidarity with Palestinians amidst the conflict in Gaza and as a direct response to what they perceive as Israeli, US, and UK aggression. The geopolitical backdrop is complex, intertwined with regional power dynamics, the broader Iran-Saudi rivalry, and the deeply rooted Arab-Israeli conflict. The attacks represent a significant escalation in an already volatile region, transforming a localized conflict into an international maritime security threat that has profound implications for global commerce.

Key Shipping Lanes and Suez Canal Vulnerabilities

The Red Sea is not merely a body of water; it’s a critical maritime superhighway connecting the Indian Ocean to the Mediterranean Sea via the Bab-el-Mandeb Strait and the Suez Canal. This route is a lynchpin for East-West trade, handling approximately 12% of global trade volume and around 30% of global container traffic. The Suez Canal, a man-made marvel, drastically reduces transit times and costs compared to the alternative route around Africa’s Cape of Good Hope. The Houthi attacks have rendered this vital passage perilous, forcing major shipping lines to re-route their vessels. This circumvention adds thousands of nautical miles to journeys, significantly increasing fuel consumption, transit times (by 10-14 days for a round trip from Asia to Europe), and operational costs. The vulnerability of such a critical choke point underscores the fragility of global supply chains when confronted with regional geopolitical instability, leading to widespread maritime security concerns and logistical challenges.

Initial Global Economic Reactions and Market Shocks

The immediate Red Sea Shipping Crisis Impact on the global economy has been palpable and multi-faceted. One of the most direct consequences has been the sharp increase in international freight rates forecast and insurance premiums. Shipping costs from Asia to Europe, for instance, have more than doubled in some cases, directly impacting import costs for businesses and potentially contributing to inflationary pressures. Industries reliant on just-in-time supply chains, such as automotive manufacturing, electronics, and retail, have been particularly vulnerable to these global supply chain disruptions in 2024. Delays in component delivery can halt production lines, leading to stockouts and consumer price hikes. Furthermore, the re-routing around the Cape of Good Hope has led to a surge in demand for shipping capacity and crew, exacerbating existing pressures on the maritime industry. Energy markets have also reacted, with concerns over oil and gas tanker transits through the Red Sea leading to price volatility. This crisis has intensified calls for comprehensive trade route diversification strategies and a deeper analysis of global maritime vulnerabilities, as highlighted in numerous maritime risk assessment reports.

In conclusion, the Red Sea crisis is more than a regional conflict; it’s a stark reminder of the interconnectedness of geopolitics and global trade. Its repercussions are being felt from manufacturing plants to consumer markets worldwide, necessitating urgent international collaboration to secure vital shipping lanes and mitigate economic fallout.

Global Supply Chain Disruptions 2024: Far-Reaching Effects

The year 2024 has witnessed an unprecedented escalation in Red Sea Shipping Crisis Impact, triggering profound and far-reaching consequences across global supply chains. What began as a regional security concern has quickly transmuted into a worldwide challenge, forcing a comprehensive re-evaluation of maritime logistics and global supply chain disruptions 2024. The decision by major shipping lines to re-route vessels around the Cape of Good Hope has not only added thousands of nautical miles to journeys but has also introduced a cascade of delays, increased costs, and inventory challenges that resonate from manufacturing hubs in Asia to consumer markets in Europe and the Americas. This section delves into the specific ramifications of this crisis, detailing how re-routing, extended transit times, and surging freight rates are impacting various industries and consumer behavior, while also offering a forward look into the potential landscape of 2025.

1. Increased Transit Times and Delivery Delays

The primary and most immediate effect of the Red Sea disruptions is the significant increase in transit times for goods traveling between Asia and Europe. Vessels that once traversed the Suez Canal, a vital artery for global trade, are now forced to navigate the much longer route around the Cape of Good Hope at Africa’s southern tip. This detour adds an estimated 7-20 days to a typical journey, translating into substantial delivery delays for a vast array of products. From automotive components and electronic gadgets to fashion apparel and perishable goods, industries reliant on just-in-time (JIT) inventory systems are struggling to adapt. Manufacturing schedules are being pushed back, product launches are delayed, and the flow of raw materials is being hampered, creating a ripple effect that impacts production lines and ultimately, the availability of goods on store shelves. The longer voyages also tie up vessels and containers for extended periods, contributing to equipment shortages and further exacerbating scheduling complexities across the entire shipping network.

2. Inventory Management Challenges and Stockouts

The protracted transit times have directly challenged traditional inventory management strategies, particularly the lean and efficient JIT models widely adopted to minimize holding costs. Companies are now faced with the imperative to carry larger buffer stocks to mitigate the risk of stockouts, a move that requires significant capital investment in warehousing, insurance, and working capital. This shift away from lean inventories increases operational costs and reduces financial flexibility. For businesses unable or unwilling to absorb these extra costs, stockouts become an imminent threat, leading to lost sales, damaged brand reputation, and dissatisfied customers. The unpredictability introduced by the crisis also makes demand forecasting more complex, as lead times become variable and less reliable. Furthermore, industries dealing with seasonal goods or products with short shelf lives, such as fresh produce or fast fashion, face heightened risks of obsolescence or spoilage during extended transits, further compounding inventory challenges and driving up waste.

3. Regional Economic Impacts (e.g., Europe, Asia, US)

The Red Sea Shipping Crisis has distinct and varied economic impacts across key global regions. Europe is arguably the most directly affected, as its supply chains are heavily intertwined with Asian manufacturing via the Suez Canal. European consumers are experiencing higher prices due to increased shipping costs, contributing to inflationary pressures, while European manufacturers face delays in receiving critical inputs and exporting finished goods. This threatens the competitiveness of European industries and could dampen economic recovery prospects. For Asia, particularly export-oriented economies like Vietnam, China, and South Korea, the crisis means higher freight rates for their goods destined for Western markets. This can erode profit margins for exporters and potentially shift sourcing decisions for global buyers. Robust Maritime risk assessment report mechanisms are crucial for Asian nations to navigate these volatile conditions. The United States, while less directly reliant on the Suez Canal for its primary trade lanes with Asia (which often cross the Pacific), still feels the ripple effects. Global container shortages, increased demand for alternative shipping routes, and the general upward pressure on International freight rates forecast globally contribute to higher import costs and potential delays for American businesses and consumers. Looking ahead to 2025, the crisis is accelerating interest in Trade route diversification strategies and nearshoring/friendshoring initiatives as businesses seek to build more resilient supply chains. According to UNCTAD’s analysis of global maritime trade patterns, the ongoing disruptions underscore the urgent need for robust contingency planning and international cooperation to safeguard global commerce against such vulnerabilities.

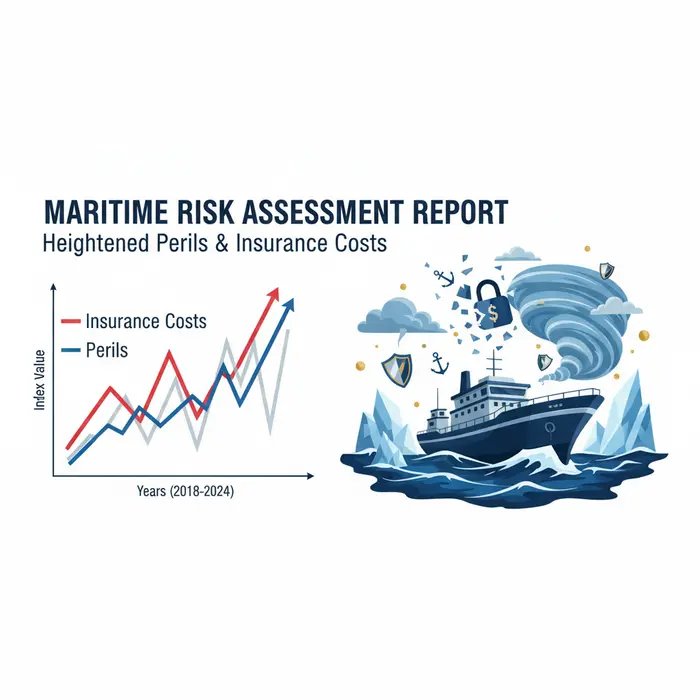

Maritime Risk Assessment Report: Heightened Perils & Insurance Costs

The global maritime industry faces unprecedented volatility, dramatically reshaping risk assessments. The Red Sea Shipping Crisis Impact, driven by Houthi aggressions, has rendered a vital trade artery perilously unsafe. This escalating geopolitical tension has triggered significant global supply chain disruptions 2024, forcing shipping companies to re-evaluate routes, adjust strategies, and confront rising financial burdens. This report analyzes elevated maritime risks, evolving maritime risk assessment report methodologies, soaring insurance premiums, and the necessity for enhanced security to protect vessels and cargo.

Elevated Geopolitical and Security Risks for Vessels

The Red Sea and Gulf of Aden have become flashpoints for severe security threats, primarily from drone and missile attacks orchestrated by Houthi militants. This direct military threat forces a dramatic re-evaluation of security protocols and operational routes. Vessels traditionally transiting the Suez Canal now frequently divert around the Cape of Good Hope. This alternative, while avoiding immediate danger, significantly extends voyage durations by 10-14 days, increasing fuel consumption, emissions, and operational costs. This rerouting exacerbates global supply chain disruptions 2024, creating bottlenecks, delays, and impacting inventory. The human element of risk has also surged, with the psychological and physical danger to seafarers becoming a critical concern. Furthermore, the incident-driven nature of these threats demands dynamic, real-time intelligence for accurate maritime risk assessment report updates, a stark contrast to previous, more predictable risk landscapes.

Impact on Shipping Insurance Premiums and War Risk Zones

The most tangible financial repercussion of the Red Sea crisis is the exponential surge in shipping insurance premiums, particularly for war risk coverage. Insurers have reclassified the Red Sea and surrounding waters as “war risk zones,” imposing substantial Additional Premium Charges (APCs). These APCs, adding hundreds of thousands of dollars per voyage, reflect the drastically elevated probability of vessel damage, crew injury, or total loss. As reported by S&P Global Market Intelligence, war risk premiums for Red Sea transits have surged by more than 1,000% for some routes. This dramatic increase in operational costs is passed down the supply chain, directly influencing the international freight rates forecast, pushing them upwards and contributing to global inflationary pressures. Marine insurance costs now fundamentally alter the economic viability of traditional shipping routes, prompting carriers to absorb higher costs or seek alternative, longer paths.

Safety and Security Protocols for Commercial Shipping

In response to these unprecedented threats, commercial shipping operations are overhauling safety and security protocols, from passive defensive strategies to active deterrence. This includes increased vessel hardening, such as reinforced bridge windows and citadels, alongside deploying trained Private Contracted Armed Security Personnel (PCASP) in high-risk areas. Advanced surveillance technologies, real-time threat intelligence sharing via military and maritime security organizations, and rigorous crew training for emergency procedures are now indispensable. Companies are investing more in comprehensive maritime risk assessment report frameworks that integrate geopolitical analysis, naval intelligence, and dynamic threat modeling. Moreover, this crisis accelerates the exploration and implementation of trade route diversification strategies, fostering greater flexibility and resilience in global logistics networks. This includes exploring alternative multimodal transport and investing in regional hubs to mitigate over-reliance on vulnerable maritime choke points.

The ongoing Red Sea crisis marks a critical juncture for the maritime industry, demanding profound adaptation and strategic foresight. From dynamic risk assessments and navigating prohibitive insurance costs to implementing stringent security measures and fostering trade route diversification strategies, stakeholders must collaborate for resilient and secure global supply chains. The repercussions of the Red Sea Shipping Crisis Impact extend beyond immediate delays, necessitating long-term commitment to enhancing maritime safety and stability in an increasingly complex world.

International Freight Rates Forecast: Volatility and Inflation

The Red Sea Shipping Crisis Impact has emerged as a significant disruptor to global trade, injecting fresh volatility and inflationary pressures into international freight markets. Ongoing attacks by Houthi militants in the vital Bab el-Mandeb Strait have forced major shipping lines to reroute vessels around Southern Africa’s Cape of Good Hope. This dramatic shift not only extends transit times by 10-14 days but also significantly increases operational costs, fundamentally altering the landscape for global supply chains in 2024. Businesses worldwide are grappling with the direct consequences, from escalating shipping fees to delays in inventory replenishment, necessitating a re-evaluation of global supply chain disruptions 2024 and the imperative for robust trade route diversification strategies.

1. Surging Container and Air Freight Costs Analysis

The immediate and most visible impact of the Red Sea crisis has been the sharp escalation in both container and air freight costs. For maritime shipping, the detour around Africa adds thousands of nautical miles to voyages, consuming more fuel and extending vessel turnaround times. This stretched capacity, coupled with increased demand on the remaining available ships, has led to a significant spike in spot rates for key routes, particularly Asia-Europe. Reports indicate that container rates on some major lanes have more than doubled since early December 2023, with sustained pressure expected throughout Q2 and potentially into Q3 2024. Furthermore, heightened insurance premiums for vessels still traversing or near the affected zones contribute to the overall cost burden, passed directly onto shippers.

In response to extended sea transit times and the imperative for timely deliveries, businesses requiring urgent cargo movements have increasingly shifted to air freight. This diversion of demand has, in turn, placed upward pressure on air cargo rates, particularly from Asian manufacturing hubs to Europe and North America. While air freight offers speed, its higher cost per unit makes it an expensive alternative, especially for bulkier goods. The current international freight rates forecast suggests that while ocean rates might see minor fluctuations, the underlying trend remains elevated until a resolution in the Red Sea is achieved, keeping air freight as a critical, albeit pricier, contingency.

2. Fuel Price Volatility and Bunker Surcharge Impacts

Fuel is the largest variable cost for shipping lines, and the rerouting around the Cape of Good Hope dramatically amplifies consumption. Longer voyages translate directly into a greater demand for marine fuel, known as bunker fuel. While global crude oil prices have shown some volatility, geopolitical tensions in the Middle East—exacerbated by the Red Sea crisis—keep upward pressure on energy markets. Shipping companies are quick to implement or increase Bunker Adjustment Factors (BAF) or Emergency Bunker Surcharges (EBS) to recoup these additional fuel expenses. These surcharges are dynamically adjusted and can add a substantial percentage to the base freight rate, making budgeting and forecasting challenging for importers and exporters.

The combined effect of increased transit times, higher fuel consumption, and geopolitical uncertainty creates a volatile environment for bunker prices. Even if crude oil prices stabilize globally, the localized demand spikes and supply chain bottlenecks for bunker fuel in certain ports can lead to regional price disparities. This ongoing uncertainty underscores the need for continuous maritime risk assessment report analyses, as fuel price volatility directly impacts the profitability and operational stability of carriers, ultimately influencing the final cost of goods.

3. Ripple Effects on Consumer Prices and Inflation Outlook

The escalating costs across both sea and air freight are not isolated to the logistics industry; they inevitably cascade through the global economy, impacting consumer prices and the overall global inflation outlook. Businesses, facing higher import costs for raw materials, components, and finished goods, are compelled to pass a portion of these increased expenses onto consumers. Sectors particularly vulnerable include electronics, apparel, automotive parts, and various consumer durables, which rely heavily on intricate global supply chains.

While central banks globally have been battling inflation with monetary tightening, the Red Sea crisis presents a new inflationary impulse, potentially slowing the progress toward targeted inflation rates. Analysts are closely watching whether these supply-side shocks will translate into a significant and sustained increase in the Consumer Price Index (CPI), particularly for goods. The delayed arrival of goods due to longer transit times can also create inventory shortages, further exacerbating price increases as demand outstrips available supply. For businesses, meticulous planning and potentially diversifying sourcing strategies are becoming crucial to mitigate these inflationary pressures and safeguard margins against a backdrop of persistent geopolitical and economic uncertainty.

Trade Route Diversification Strategies for Business Resilience

The global supply chain landscape is perpetually evolving, marked by unforeseen disruptions that challenge conventional logistics paradigms. The recent Red Sea Shipping Crisis Impact has underscored the vulnerability of concentrated trade routes, compelling businesses worldwide to re-evaluate their operational frameworks. This surge in global supply chain disruptions 2024 necessitates a proactive approach to build resilience, moving beyond mere contingency planning to strategic diversification. Businesses must now prioritize agility, visibility, and adaptability to mitigate risks, maintain continuity, and safeguard their competitive edge amidst an increasingly volatile geopolitical and economic environment. This section explores strategic responses businesses can adopt to mitigate future disruptions, focusing on alternative trade routes, the potential for nearshoring and reshoring, and the growing importance of digitalization in enhancing supply chain visibility and resilience.

1. Exploring Alternative Shipping Corridors and Modes

The immediate fallout from the Red Sea Shipping Crisis Impact has been a significant re-routing of vessels around the Cape of Good Hope, leading to extended transit times and increased fuel costs. This situation highlights the critical need for businesses to actively explore and pre-plan alternative shipping corridors. While the Cape route offers a viable bypass, its implications on international freight rates forecast and delivery schedules are substantial. Strategically, businesses should conduct thorough maritime risk assessment report analyses for multiple routes, considering geopolitical stability, infrastructure, and potential congestion. This might involve assessing the feasibility of Arctic routes for seasonal use, or expanding partnerships with carriers operating through less conventional passages.

Beyond sea lanes, diversifying transportation modes presents another layer of resilience. For time-sensitive or high-value goods, air cargo can provide a rapid, albeit more expensive, alternative. Rail freight, especially across continents (e.g., the New Silk Road connecting Asia and Europe), offers a middle-ground solution, balancing speed and cost, reducing reliance on purely maritime routes. Developing multimodal strategies, where different segments of a journey utilize varied transport types, significantly reduces exposure to single-point failures. This approach requires intricate logistical planning and strong partnerships with a diverse range of freight forwarders and carriers, ensuring flexibility to pivot rapidly when disruptions arise. Understanding these options is paramount for effective trade route diversification strategies.

2. Nearshoring and Reshoring Trends as Mitigation

The pursuit of cost efficiency often led companies to offshore manufacturing to distant regions, creating elongated and vulnerable supply chains. The recent wave of global supply chain disruptions 2024 has accelerated the trends of nearshoring and reshoring, positioning production closer to consumer markets or back to the home country. Nearshoring, moving production to neighboring countries, offers benefits like reduced transportation costs and transit times, improved inventory management, and better communication. Reshoring, on the other hand, brings manufacturing back to the domestic market, offering enhanced control over quality, intellectual property, and often benefiting from government incentives and a skilled local workforce.

These strategies contribute significantly to supply chain resilience by shortening the physical distance goods must travel, thereby reducing exposure to international maritime risks and geopolitical uncertainties. While initial investment costs and potential labor shortages can be challenges, the long-term gains in agility, responsiveness, and reduced carbon footprint often outweigh them. Businesses adopting these strategies are effectively building buffer zones against future crises, creating more robust regional supply networks less susceptible to distant shocks. This strategic shift is not just about logistics; it’s about rebuilding trust and control within the supply chain. A recent report by the World Economic Forum on supply chain resilience highlights the growing imperative for localized production to safeguard against future shocks.

3. Leveraging Digitalization for Supply Chain Visibility and Resilience

In an era defined by rapid change, real-time data and predictive analytics are no longer luxuries but necessities for supply chain management. Digitalization plays a pivotal role in enhancing supply chain visibility and resilience, offering tools that transform reactive responses into proactive strategies. Technologies such as Artificial Intelligence (AI), the Internet of Things (IoT), blockchain, and advanced analytics enable businesses to gain end-to-end visibility of their goods in transit, monitor supplier performance, and anticipate potential disruptions. IoT sensors can track cargo location, temperature, and humidity, providing critical data for risk assessment. AI-powered platforms can analyze vast datasets to identify patterns, forecast demand fluctuations, and predict potential bottlenecks or delays before they materialize.

Blockchain technology offers an immutable, transparent ledger for transactions and movements, enhancing trust and traceability across complex supply networks. This is particularly valuable for verifying ethical sourcing, combating counterfeiting, and streamlining customs processes. Furthermore, digital twin technology can create virtual models of the supply chain, allowing businesses to simulate various disruption scenarios and test mitigation strategies without real-world consequences. By leveraging these digital tools, companies can make more informed decisions, optimize inventory levels, manage supplier relationships more effectively, and rapidly pivot their logistics operations in response to unforeseen events. The comprehensive understanding provided by digitalization is invaluable in navigating complex challenges like the Red Sea Shipping Crisis Impact, allowing businesses to stay ahead of the curve and maintain competitive advantage.

In conclusion, the volatile nature of global trade demands a multi-pronged approach to supply chain resilience. By strategically diversifying trade routes, embracing nearshoring and reshoring, and comprehensively leveraging digitalization, businesses can transform vulnerabilities into strengths. These strategies, when integrated effectively, create agile, responsive, and robust supply chains capable of withstanding the next wave of disruptions, ensuring sustained operations and continued growth in an unpredictable world.

Partner with Vietnam’s Leading Suppliers

Looking for reliable suppliers in Vietnam? Contact VietnamSuppliers.com today to connect with verified manufacturers and exporters across all industries.

—————————————

References

– UNCTAD warns of global impact as Red Sea crisis escalates: https://unctad.org/press-material/unctad-warns-global-impact-red-sea-crisis-escalates-and-panama-canal-challenges

– :

– War risk premiums surge for Red Sea transits: https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/war-risk-premiums-surge-for-red-sea-transits-80979803

– IMF Blog: The Red Sea Attacks: Understanding the Economic Impact: https://www.imf.org/en/Blogs/Articles/2024/01/30/the-red-sea-attacks-understanding-the-economic-impact

– World Economic Forum on supply chain resilience: https://www.weforum.org/agenda/2023/01/supply-chains-resilience-manufacturing-risks-recession-inflation/