What is an International Letter of Credit (ILOC)?

An International Letter of Credit (ILOC) stands as a cornerstone in the intricate world of global trade finance. It serves as a vital financial instrument designed to mitigate the inherent risks associated with cross-border transactions, providing a robust framework of trust and security for both buyers (importers) and sellers (exporters) operating across different jurisdictions. In essence, an ILOC is a commitment from a bank on behalf of a buyer that payment will be made to the seller, provided that the seller presents specific, compliant shipping documents within a stipulated timeframe. This banking undertaking dramatically reduces the uncertainty that often plagues international dealings, transforming potential high-risk ventures into manageable and secure exchanges. By ensuring that goods are shipped as agreed and payment is guaranteed, the International Letter of Credit facilitates smoother and more reliable commerce worldwide.

1. Defining ILOC: A Core Trade Finance Tool

At its heart, an International Letter of Credit (ILOC), often simply referred to as a Letter of Credit (LC) in international contexts, is a financial guarantee issued by a bank. This guarantee is provided to an exporter (beneficiary) on behalf of an importer (applicant), promising payment for goods or services delivered, provided the exporter complies strictly with the terms and conditions outlined in the LC. Unlike a simple promise to pay, an ILOC shifts the payment obligation from the buyer to a reputable financial institution, significantly reducing the seller’s payment risk. It acts as a contractual agreement where the issuing bank substitutes its creditworthiness for that of its client (the buyer), offering a secure payment mechanism crucial for bridging geographical and trust gaps between trading partners. The core principle revolves around document compliance: payment is made against documents, not against physical goods. This documentary nature makes the Letter of Credit process highly standardized and predictable, adhering to globally recognized rules such as the Uniform Customs and Practice for Documentary Credits (UCP) published by the International Chamber of Commerce (ICC). These standardized Types of Letter of Credit ensure consistency and understanding across diverse legal and banking systems, making it an indispensable tool for Letter of Credit for import export.

2. Key Parties Involved in an ILOC Transaction

Understanding the various roles in an International Letter of Credit transaction is essential for grasping its operational mechanics. Typically, four primary parties are involved, though additional intermediaries can participate to enhance security or facilitate processes:

- Applicant (Importer/Buyer): This is the party requesting the ILOC from their bank. They are responsible for initiating the process and ensuring the terms of the LC align with the underlying sales contract.

- Beneficiary (Exporter/Seller): The party who will receive payment under the ILOC, provided they meet all stipulated conditions and present the required documents.

- Issuing Bank (Buyer’s Bank): The financial institution that issues the ILOC at the request of the applicant. This bank undertakes the primary obligation to pay the beneficiary, provided the documents are compliant.

- Advising Bank (Seller’s Bank): Usually a bank in the beneficiary’s country, it verifies the authenticity of the ILOC and advises the beneficiary of its terms. It does not carry a payment obligation but acts as a communication channel.

Beyond these core players, a Confirming Bank may also be involved. This bank, often in the beneficiary’s country, adds its own guarantee to the issuing bank’s guarantee, taking on the payment risk of the issuing bank. This additional layer of security is particularly valuable when the issuing bank is located in a country perceived as having higher political or economic risk, or when the beneficiary prefers the security of a local bank’s undertaking. The entire Letter of Credit process is meticulously documented, ensuring transparency and accountability at every stage.

3. Benefits for Importers and Exporters

The widespread adoption of the International Letter of Credit in global commerce stems from its significant advantages for both sides of a transaction.

For Exporters (Sellers):

The primary benefit for an exporter is the near-guarantee of payment. Once the exporter ships the goods and presents the exact documents specified in the ILOC to the advising or confirming bank, they are assured of receiving payment from the issuing bank (or confirming bank). This eliminates concerns about the buyer’s creditworthiness or solvency, political instability in the buyer’s country, or currency exchange risks in some cases. It significantly mitigates the risk of non-payment, allowing exporters to confidently enter new markets and expand their international reach. Furthermore, by securing an ILOC, exporters can often access pre-shipment or post-shipment financing from their banks against the strength of the bank’s commitment, improving cash flow. While the standard ILOC focuses on payment, related instruments like a Standby Letter of Credit (SBLC) offer a safety net for contractual performance rather than a direct payment mechanism for goods, acting more like a guarantee.

For Importers (Buyers):

While often perceived as primarily benefiting sellers, ILOCs offer substantial advantages to buyers as well. An importer is assured that payment will only be released when the exporter has met all the documentary conditions specified in the ILOC. This means the importer retains control, knowing that the goods have been shipped, relevant inspections conducted, and necessary permits obtained before their bank makes payment. This protection against non-performance or non-delivery of goods as per contract terms is invaluable. It also enables importers to negotiate better terms with suppliers who might otherwise demand upfront payment without such a guarantee. The secure International Letter of Credit transactions mechanism therefore balances the interests of both parties, fostering trust and enabling efficient Letter of Credit for import export operations.

Types of Letter of Credit: A Comprehensive Overview

The International Letter of Credit (LC) stands as a cornerstone in global trade, offering a secure payment mechanism that bridges the trust gap between importers and exporters. Navigating the diverse landscape of global commerce necessitates a clear understanding of the various types of Letter of Credit, each designed to meet specific transactional needs and risk profiles. From guaranteeing payment to offering pre-shipment finance, LCs facilitate seamless Letter of Credit for import export operations by mitigating risks for both parties involved in international trade. Let’s delve into the specific characteristics and applications of these vital financial instruments.

1. Revocable vs. Irrevocable Letters of Credit

This fundamental distinction lies at the heart of an LC’s security. A Revocable Letter of Credit, as the name suggests, can be amended or cancelled by the issuing bank without prior notice to the beneficiary (exporter). This type offers minimal security to the seller, making it extremely rare in international trade due to the inherent risks. Exporters have little assurance of payment if the LC can be withdrawn at any time before payment is made. Consequently, revocable LCs are almost never used in practice where the beneficiary requires firm payment assurance.

In stark contrast, an Irrevocable Letter of Credit cannot be amended or cancelled without the explicit agreement of all parties involved: the applicant (importer), the issuing bank, and the beneficiary. This provides a significantly higher level of security for the exporter, as it guarantees that once the LC is issued and compliant documents are presented, payment will be made. The vast majority of LCs used in international transactions today are irrevocable, as mandated by the Uniform Customs and Practice for Documentary Credits (UCP), ensuring stability and predictability in the Letter of Credit process.

2. Confirmed vs. Unconfirmed Letters of Credit

This distinction introduces an additional layer of security, particularly relevant when dealing with less familiar banks or countries perceived to have higher economic or political risks. An Unconfirmed Letter of Credit carries only the promise of the issuing bank to honor payment, provided all terms and conditions are met. The advising bank, which communicates the LC to the beneficiary, does not add its own undertaking to pay. This means the beneficiary’s payment assurance rests solely on the creditworthiness and reliability of the issuing bank.

A Confirmed Letter of Credit, however, provides an additional, independent undertaking by a second bank (the confirming bank), usually located in the exporter’s country. The confirming bank adds its own guarantee to pay the beneficiary, even if the issuing bank defaults on its payment obligation. This significantly enhances the security for the exporter, as they now have two banks obligated to pay. This added security often comes with an additional fee charged by the confirming bank. This type is particularly advantageous for exporters dealing with new buyers, in countries with unstable banking systems, or where the credit rating of the issuing bank is unknown or low. The International Chamber of Commerce (ICC) provides comprehensive guidelines on these instruments, underpinning their global acceptance and reliability, often detailed in publications like the UCP 600 which governs most LCs globally. For a deeper understanding of these banking practices, resources like Investopedia on Confirmed Letters of Credit offer valuable insights.

3. Sight, Usance, and Red Clause Letters of Credit

These types differentiate LCs based on the timing and mechanism of payment to the beneficiary:

- Sight Letter of Credit: This is the most straightforward and fastest payment method. Under a Sight LC, payment is made immediately (or “at sight”) upon the presentation of compliant shipping documents to the nominated bank. Once the documents are verified to meet all terms and conditions of the LC, the bank makes the payment without any delay, offering instant liquidity to the exporter.

- Usance Letter of Credit (Time Letter of Credit): Unlike a Sight LC, a Usance LC specifies a deferred payment period. Payment is not made immediately but after a predetermined period, often 30, 60, 90, or 120 days, from the date of the bill of lading, the date of presentation of documents, or another specified event. This effectively provides a credit period to the importer, allowing them to receive and potentially sell the goods before making payment. For the exporter, this means a delay in receiving funds, though the payment is still guaranteed by the banks involved. This type is common when importers require time to manage their cash flow or prepare for customs clearance and onward distribution.

- Red Clause Letter of Credit: This unique type allows the beneficiary to receive a portion of the LC value as an advance payment from the nominated bank *before* shipment of goods and presentation of the full set of shipping documents. The “red clause” historically referred to a clause written in red ink, indicating this special condition. This pre-shipment finance facility is incredibly useful for exporters who need funds to purchase raw materials, manufacture goods, or cover other pre-export costs. The advance is essentially an unsecured loan from the nominated bank, guaranteed by the issuing bank. The issuing bank, in turn, holds the applicant (importer) responsible for the advance if the exporter fails to ship the goods or present compliant documents.

Beyond these, other specialized LCs exist, such as the Standby Letter of Credit, which acts more as a guarantee against non-performance rather than a primary payment mechanism. Each type of Letter of Credit plays a critical role in facilitating international trade, providing tailored solutions for various financial and logistical requirements across the globe.

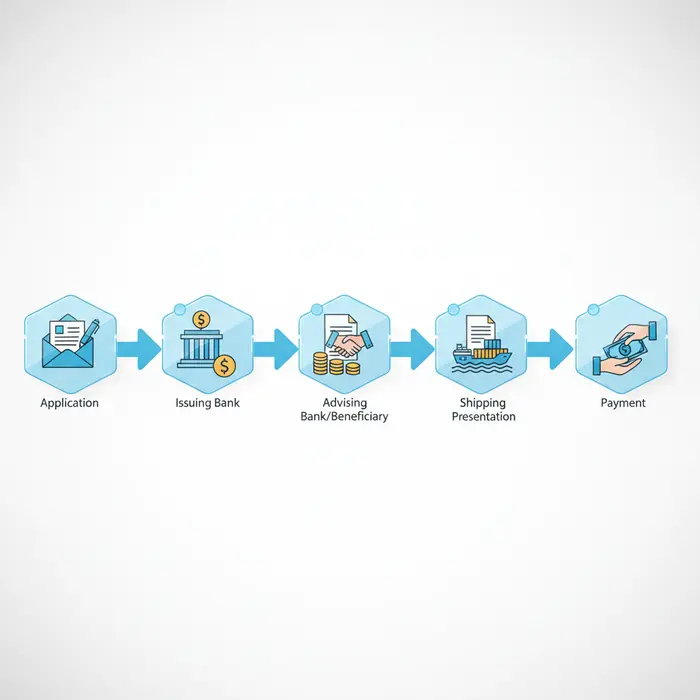

The International Letter of Credit (ILOC) is a fundamental financial instrument in global trade, offering unparalleled security for both importers and exporters. It acts as a commitment from a bank (the issuing bank) to make a payment to a beneficiary (the exporter) on behalf of a client (the importer), provided that the exporter presents specific, compliant documents. Understanding the **Letter of Credit process** is crucial for efficient and secure international transactions. This guide will demystify the journey of an ILOC, from initial application to final payment, ensuring clarity for all participants in a typical **Letter of Credit for import export** scenario. While various types of Letter of Credit exist, including the **Standby Letter of Credit** (SBLC), the core transactional LC follows a predictable and robust sequence.

1. Initiation and Application by the Importer

The journey of an International Letter of Credit begins with the importer, who wishes to purchase goods from an exporter. After negotiating the sales contract, which typically stipulates payment via an ILOC, the importer approaches their bank, known as the issuing bank. The importer submits an application requesting the issuance of an LC in favor of the exporter. This application is a critical document, detailing all the terms and conditions under which the payment will be made. It specifies the LC amount, currency, beneficiary’s details, a detailed description of goods, required shipping documents (e.g., commercial invoice, packing list, bill of lading, certificate of origin, inspection certificates), latest shipment and expiry dates, and any special conditions. The importer must have a credit line or sufficient funds. The issuing bank reviews the application against the importer’s creditworthiness and the proposed terms. Accuracy at this stage is paramount, as discrepancies can lead to significant delays and complications later in the **Letter of Credit process**.

2. Issuance and Advising by Banks

Once the issuing bank approves the importer’s application, it officially issues the International Letter of Credit, a formal undertaking to pay the exporter if all specified conditions are met. The issuing bank then transmits the LC to an advising bank in the exporter’s country. This advising bank, often a correspondent, verifies the LC’s authenticity and formally notifies the exporter (beneficiary). The advising bank’s role is primarily to inform, not to undertake payment obligation unless it also acts as a confirming bank.

For added security, especially in higher-risk contexts, the exporter may request a **confirmed Letter of Credit**. Here, a **confirming bank** (which can be the advising bank or another) adds its own undertaking, guaranteeing payment. This provides two bank guarantees. The exporter meticulously reviews the received LC to ensure all terms align with the sales contract. Any discrepancies must be immediately communicated to the importer for amendment before goods are shipped, preventing potential issues in the **Letter of Credit for import export** transaction.

3. Presentation of Documents by the Exporter

With a verified and acceptable International Letter of Credit, the exporter manufactures and ships goods as per the sales contract. Following shipment, the critical phase of **presentation of documents** begins. The exporter gathers all documents precisely as stipulated in the LC, typically including: Commercial Invoice, Packing List, Bill of Lading (or other transport document), Certificate of Origin, Insurance Certificate, Inspection Certificate, and a Draft. Each document must strictly conform to the LC requirements, adhering to ‘strict compliance’; even minor discrepancies can delay or refuse payment.

The exporter presents these documents to the **negotiating bank** (often the advising or confirming bank) within the LC’s validity period. The negotiating bank examines them for compliance. If compliant, it honors the LC by paying the exporter or purchasing the documents and forwarding them to the issuing bank. The issuing bank, upon receiving compliant documents, examines them again. If satisfied, it releases payment to the negotiating bank and debits the importer’s account. The issuing bank then forwards the original documents to the importer, who needs these (especially the bill of lading) to take possession of the goods upon arrival. This final step concludes the payment cycle of the **Letter of Credit process**, ensuring both parties fulfill their obligations under the secured transaction.

Standby Letter of Credit (SBLC): A Guarantee for Performance

In the complex world of global commerce, trust and assurance are paramount. While an International Letter of Credit typically facilitates primary payment for goods, the Standby Letter of Credit (SBLC) plays a distinct, yet equally critical, role. This financial instrument acts as a secondary payment mechanism or performance guarantee, providing a crucial safety net for non-trade obligations. It assures a beneficiary that if an applicant fails to meet contractual commitments, a bank will step in to cover the financial shortfall, thereby mitigating risk and fostering confidence in a wide array of business transactions, particularly in cross-border dealings and large-scale projects.

1. Understanding the SBLC: More Than a Payment Tool

The Standby Letter of Credit (SBLC) is a versatile financial instrument issued by a bank on behalf of its client (the applicant) to a third party (the beneficiary). Unlike a traditional Commercial Letter of Credit, which is generally expected to be drawn upon as the primary payment for goods, an SBLC serves primarily as a contingent payment mechanism or a performance guarantee. Its “standby” nature means it is only activated or “drawn upon” if the applicant fails to fulfill a specific contractual obligation, whether it’s a payment, a performance, or a regulatory compliance requirement. In essence, it acts as a robust form of assurance, ensuring that the beneficiary will be compensated financially if the applicant defaults on their commitments. This makes the SBLC an invaluable tool for mitigating risk, particularly in high-value contracts, long-term projects, and import export scenarios where unforeseen challenges can arise.

2. Key Differences from Commercial Letters of Credit

To truly grasp the significance of an SBLC, it’s essential to differentiate it from its more common counterpart, the Commercial Letter of Credit (CLC). While both are types of Letter of Credit and involve banks guaranteeing payment, their fundamental roles diverge significantly. A CLC is designed as the primary payment method for a transaction, typically involving the sale of goods. It is almost always expected to be drawn upon when the seller presents documents proving shipment. The Letter of Credit process for a CLC focuses on document compliance (e.g., bills of lading, invoices) to trigger payment.

In contrast, an SBLC is a secondary payment mechanism. It is a safety net, an insurance policy of sorts, that is intended to be activated only in the event of a default or non-performance by the applicant. Payment under an SBLC is triggered by the beneficiary’s assertion that the applicant has failed to meet their contractual obligations, often supported by minimal documentation such as a simple declaration of default. Therefore, a key distinction lies in the probability of being drawn upon: CLCs are usually drawn, whereas SBLCs are ideally never drawn upon, their mere existence serving as sufficient leverage and assurance. This makes the SBLC particularly suitable for securing non-trade obligations like loans, leases, or project completion guarantees, where the underlying intent is not direct payment for goods, but assurance against failure.

3. Applications of SBLC in Various Industries

The versatility of the Standby Letter of Credit makes it an indispensable tool across a multitude of industries, extending far beyond traditional import export trade. Its capacity to provide a robust performance guarantee or backstop payment solution is highly valued.

- Construction and Infrastructure: SBLCs are frequently used as performance bonds, guaranteeing that a contractor will complete a project according to agreed-upon terms and schedule. They can also serve as advance payment guarantees, assuring that initial funds provided to a contractor will be used as intended.

- Energy and Commodity Trading: In long-term supply contracts for oil, gas, or other commodities, an SBLC can secure future payments, ensuring that buyers fulfill their purchase commitments and suppliers are compensated even if the buyer faces financial difficulties.

- International Trade and Finance: Beyond primary payment, SBLCs can secure various trade-related obligations such as bid bonds for tenders, warranty guarantees, and obligations related to customs duties or port charges. They also play a role in loan syndications, securing repayment to lenders, and supporting the issuance of commercial paper.

- Real Estate: Landlords may require an SBLC from tenants as a form of security deposit, guaranteeing lease payments or adherence to lease terms, especially for commercial properties or long-term rentals.

- Government Contracts: Entities bidding on large government projects often use SBLCs to meet stringent financial guarantee requirements, ensuring their ability to fulfill the contract if awarded.

These diverse applications highlight the SBLC’s crucial role as a flexible and potent financial instrument, providing a layer of security that underpins trust and facilitates complex transactions across the global economy.

Leveraging Letter of Credit for Import Export Success

The complexities of global trade demand robust financial instruments to ensure security and trust between parties. The International Letter of Credit (ILOC) stands as a cornerstone in this regard, offering an indispensable mechanism for importers and exporters alike. Effectively utilizing ILOCs can significantly de-risk transactions, streamline operations, and pave the way for successful international expansion. This section will delve into strategic insights for businesses to harness the full potential of LCs, transforming them from mere payment tools into powerful facilitators of global commerce. Understanding the nuances of the Letter of Credit for import export is crucial for navigating diverse international markets.

1. Risk Mitigation Strategies for International Trade

International trade is inherently fraught with risks, from payment defaults and non-delivery of goods to political instability and currency fluctuations. An International Letter of Credit fundamentally addresses the payment risk for the exporter and performance risk for the importer. For exporters, an LC guarantees payment from a reputable bank, provided all documentary conditions are met, shifting the credit risk from the buyer to the issuing bank. This assurance enables businesses to confidently expand into new, potentially high-risk markets. Conversely, importers gain assurance that payment will only be released once the specified goods have been shipped and all required documents – verifying quantity, quality, and shipping details – are presented. This structured process mitigates the risk of receiving substandard goods or non-delivery. Furthermore, LCs can be structured to include specific inspection certificates or third-party verification, adding another layer of security. Mastering the Letter of Credit process is key to leveraging these protections.

2. Choosing the Right LC Type for Your Transaction

The landscape of Letters of Credit is diverse, with various types of Letter of Credit tailored to specific transactional needs. Selecting the appropriate type is critical for optimizing security and efficiency.

- Irrevocable Letter of Credit: This is the most common type, meaning it cannot be amended or cancelled without the consent of all parties, providing maximum security.

- Confirmed Letter of Credit: For transactions involving higher risk or less familiar banks, an exporter might request a confirmed LC. Here, a second bank (the confirming bank, typically in the exporter’s country) adds its guarantee to the issuing bank’s, providing an additional layer of payment assurance.

- Sight vs. Usance Letter of Credit: A sight LC requires immediate payment upon presentation of compliant documents, while a usance LC (or time LC) allows for payment at a future date, offering credit terms to the buyer, often against an acceptance or deferred payment undertaking.

- Standby Letter of Credit (SBLC): Unlike commercial LCs which are primary payment mechanisms, a Standby Letter of Credit acts as a secondary payment method or a guarantee. It is called upon only if the applicant fails to fulfill a contractual obligation, such as defaulting on a loan or failing to perform under a service contract. SBLCs are highly flexible and can secure various financial and performance obligations, making them an invaluable tool for different trade scenarios.

Understanding these variations empowers businesses to choose the most suitable instrument, enhancing trust and facilitating smoother trade relations. For more details on trade finance instruments, the International Chamber of Commerce (ICC) provides comprehensive resources on documentary credits.

3. Common Pitfalls and How to Avoid Them

While highly secure, LCs are not without their complexities. Common pitfalls primarily revolve around document discrepancies, which can delay payment or even lead to rejection.

- Document Discrepancies: This is the most frequent issue. Even minor errors—such as misspelled names, incorrect product descriptions, or inconsistent dates across documents (e.g., invoice, bill of lading, packing list)—can lead banks to declare documents non-compliant. To avoid this, meticulous attention to detail is paramount. Exporters must ensure all documents strictly adhere to the LC terms, down to the last comma. A robust internal checklist and a thorough pre-shipment document review process are essential.

- Understanding UCP 600: The Uniform Customs and Practice for Documentary Credits (UCP 600) issued by the ICC governs most LCs globally. Parties involved must have a clear understanding of these rules to ensure compliance and avoid misinterpretations. Familiarity with UCP 600 empowers businesses to negotiate LC terms effectively and handle discrepancies proactively.

- Bank Charges: LC transactions incur various bank charges (issuing, advising, confirming, discrepancy fees). These charges can add up, and it’s crucial for both parties to clarify who bears which costs during contract negotiation.

- Timeliness: Adherence to stipulated presentation periods and latest shipment dates is critical. Delays can result in discrepancies and forfeiture of payment rights. Proactive communication with freight forwarders and banks is vital.

By being acutely aware of these potential pitfalls and implementing rigorous internal controls, businesses can significantly reduce the risk of complications, ensuring the smooth execution of their International Letter of Credit transactions and optimizing their Letter of Credit for import export operations.

Harnessing the strategic power of the International Letter of Credit is no longer just a safeguard but a competitive advantage in global trade. By understanding its various types, implementing robust risk mitigation strategies, and proactively avoiding common pitfalls, businesses can secure their transactions, foster trust with international partners, and confidently expand their reach into new markets. The ILOC, therefore, remains an indispensable tool for achieving import-export success and sustainable growth.

Partner with Vietnam’s Leading Suppliers

Looking for reliable suppliers in Vietnam? Contact VietnamSuppliers.com today to connect with verified manufacturers and exporters across all industries.

—————————————

References

– International Letter of Credit: https://www.investopedia.com/terms/l/letterofcredit.asp

– Investopedia on Confirmed Letters of Credit: https://www.investopedia.com/terms/c/confirmed-letter-of-credit.asp

– Letter of Credit (LC) Definition, Types, and Example: https://www.investopedia.com/terms/l/letterofcredit.asp

– Standby Letter of Credit: https://www.investopedia.com/terms/s/standbyletterofcredit.asp

– International Chamber of Commerce (ICC) resources on documentary credits: https://iccwbo.org/trade-facilitation/documentary-credits/