Introduction to Cash Against Documents (CAD)

In the intricate world of global commerce, selecting the appropriate payment method is paramount for mitigating risks and ensuring smooth transactions for both exporters and importers. Among the various mechanisms designed to facilitate international trade, Cash Against Documents (CAD) stands out as a commonly utilized and often misunderstood option. This method, while offering a balance between risk and simplicity, plays a crucial role as a key international trade payment method, particularly when there’s an established trust between trading partners or for transactions where the costs of more complex arrangements are prohibitive. Understanding the nuances of CAD is essential for businesses looking to expand their reach across borders, providing clarity on how it functions, its advantages, and its inherent limitations within the broader landscape of export payment terms for buyers.

1. What is Cash Against Documents (CAD)?

Cash Against Documents (CAD) is an international trade payment method where an exporter (seller) ships goods to an importer (buyer) and then entrusts the shipping and other essential documents to their bank (the remitting bank). These documents are not released directly to the importer until the importer pays for the goods, usually through their own bank (the collecting bank). Essentially, the importer obtains possession of the documents – such as the bill of lading, commercial invoice, packing list, and certificate of origin – only after making the full payment. Without these documents, the importer cannot take possession of the goods at the destination port. This mechanism provides a certain level of security for the exporter, as they retain control over the goods until payment is confirmed, while offering the importer the assurance that goods have been shipped before payment is made. It’s a fundamental aspect of many Cash Against Documents Payment Terms arrangements, balancing the interests of both parties in a transactional setting.

2. How CAD Fits into International Trade Payment Methods

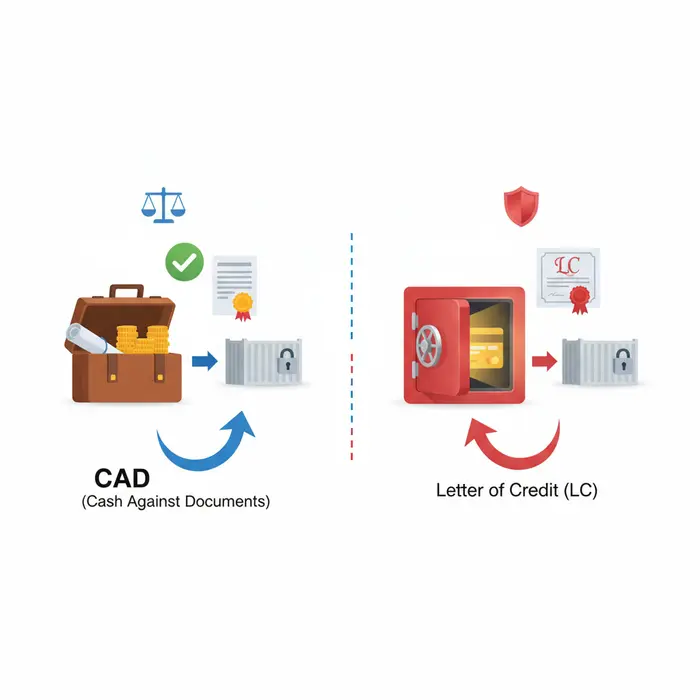

Within the spectrum of international trade payment methods, CAD typically occupies a middle ground in terms of security and cost, positioned between the higher risk of ‘open account’ transactions for exporters and the higher security and complexity of Letters of Credit (LCs). For many businesses, particularly those engaged in repeat transactions or operating in markets with reasonable political and economic stability, CAD offers a pragmatic solution. Its relatively lower cost and simpler procedure make it an attractive option compared to the more elaborate and expensive Letter of Credit. While an LC offers an independent payment guarantee from a bank, significantly reducing exporter risk, CAD relies more on the willingness of the importer’s bank to collect payment before releasing documents. Consequently, in the debate of CAD vs Letter of Credit, CAD provides less security for the exporter than an LC, as the collecting bank acts as a facilitator rather than a guarantor of payment. However, for buyers, CAD can be preferable as it avoids the need to tie up credit lines for an LC and grants them control over the goods once payment is made, making it an appealing choice among export payment terms for buyers who prefer a simpler, less restrictive process.

3. Key Parties Involved in a CAD Transaction

Understanding the operational flow of a Cash Against Documents procedure requires familiarity with the roles of the principal parties involved:

- The Exporter (Seller/Beneficiary): This is the party that ships the goods and initiates the CAD transaction. After shipping, the exporter prepares all necessary shipping and commercial documents and presents them to their bank for collection.

- The Importer (Buyer/Drawee): This is the party receiving the goods. The importer is responsible for making the payment to the collecting bank in exchange for the shipping documents, which are required to clear the goods from customs and take possession.

- The Remitting Bank (Exporter’s Bank): This bank receives the documents from the exporter and is responsible for forwarding them to the collecting bank, along with specific instructions for collection of payment from the importer.

- The Collecting Bank (Importer’s Bank): This bank receives the documents from the remitting bank. Its role is to present these documents to the importer, collect the specified payment according to the instructions, and then release the documents to the importer. Once payment is received, the collecting bank remits the funds back to the remitting bank, which then credits the exporter’s account.

The seamless coordination among these parties is crucial for the efficient execution of any Cash Against Documents procedure, ensuring that goods reach their destination and payment is made in a timely and secure manner.

The Cash Against Documents Procedure: A Step-by-Step Guide

In the complex world of international trade, choosing the right payment method is paramount for managing risk and ensuring smooth transactions. The Cash Against Documents (CAD) procedure stands as a common intermediary option, offering a balance between the seller’s desire for security and the buyer’s need for control. Unlike a Letter of Credit (L/C), which involves a bank’s payment guarantee, CAD relies on banks solely as facilitators for the exchange of documents against payment or acceptance. This guide details the operational flow of a CAD transaction, outlining the critical roles of both parties and the intermediary banks, making it a key element in various international trade payment methods.

1. Initiating the CAD Transaction: Seller’s Role

The journey of a CAD transaction begins with the seller. Once a sales contract is finalized, explicitly stating Cash Against Documents Payment Terms, the seller proceeds with the initial steps:

- Goods Shipment: The seller manufactures or procures the goods and arranges for their shipment to the buyer’s designated port or location. It’s crucial that the goods are shipped as per the agreed-upon terms (e.g., Incoterms).

- Document Preparation: Following shipment, the seller meticulously prepares a comprehensive set of shipping and commercial documents. These typically include the commercial invoice, packing list, certificate of origin, insurance certificate (if applicable), and most importantly, the bill of lading or airway bill, which represents title to the goods. These documents are the lynchpin of the CAD procedure, as they convey ownership and enable the buyer to take possession of the goods.

- Presentation to Remitting Bank: The seller then presents this complete set of documents to their bank, known as the Remitting Bank. Along with the documents, the seller provides clear “collection instructions.” These instructions specify the terms under which the documents are to be released to the buyer – primarily “against payment” (Documents Against Payment – D/P) or “against acceptance” (Documents Against Acceptance – D/A) of a bill of exchange.

2. Document Presentation and Negotiation by Banks

Upon receiving the documents and collection instructions from the seller, the banks play a crucial, albeit non-guaranteeing, role in facilitating the exchange:

- Remitting Bank’s Action: The seller’s bank (Remitting Bank) reviews the documents and instructions for apparent completeness and consistency. It then forwards these documents, along with its own “collection order,” to the buyer’s bank, referred to as the Collecting Bank or Presenting Bank, typically located in the buyer’s country. The Remitting Bank acts on behalf of the seller, ensuring the smooth transmission of documents.

- Collecting Bank’s Notification: Once the Collecting Bank receives the documents and collection order, its primary responsibility is to notify the buyer of their arrival. The bank then presents the documents to the buyer and requests either immediate payment (for D/P terms) or acceptance of a draft (for D/A terms), strictly adhering to the instructions received from the Remitting Bank.

- Buyer’s Examination: While banks deal solely with documents and not the goods themselves, the buyer is usually given a reasonable period to examine the documents. This examination is critical to ensure the documents conform to the sales contract and are sufficient to clear the goods from customs and claim them from the carrier. This stage highlights a key difference between CAD vs Letter of Credit, as an L/C mandates bank scrutiny of documents against L/C terms before payment, offering a layer of assurance.

3. Payment and Document Release Flowchart

The final stage of the Cash Against Documents procedure culminates in the payment or acceptance, leading to the release of documents and transfer of funds:

- Buyer’s Action:

- For Documents Against Payment (D/P): The buyer pays the full invoice amount to the Collecting Bank. This payment is typically required before any documents are released.

- For Documents Against Acceptance (D/A): The buyer “accepts” a bill of exchange (draft) by signing it, committing to pay the stated amount on a future maturity date (e.g., 30, 60, or 90 days after sight or bill of lading date).

- Document Release: Crucially, upon receiving either full payment (for D/P) or the accepted draft (for D/A), the Collecting Bank releases the original shipping documents to the buyer. These documents are indispensable for the buyer to clear the goods through customs, take delivery from the shipping company, and ultimately gain possession of the merchandise. Without these documents, the goods remain with the carrier or in customs, making this step the pivotal moment for the buyer.

- Fund Transfer (D/P): If D/P terms were used, the Collecting Bank remits the received funds, minus its own charges, to the Remitting Bank. The Remitting Bank then credits the seller’s account, after deducting its fees.

- Managing Accepted Drafts (D/A): In a D/A scenario, the Collecting Bank holds the accepted draft until its maturity date. On the due date, the bank presents the draft to the buyer for payment. Once the payment is received, the funds are then transferred back to the seller via the Remitting Bank. This extends credit to the buyer, representing a higher risk for the seller compared to D/P.

The Cash Against Documents procedure is a practical option for exporters and importers who have established trust but prefer the structured involvement of banks for document handling and payment collection. It offers a more secure method than open account terms while being less costly and complex than an L/C, making it a viable component of export payment terms for buyers and sellers in many trading relationships.

CAD vs. Letter of Credit (LC): Key Differences and When to Choose

In the intricate world of international trade, selecting the right payment method is crucial for managing risk, ensuring timely payment, and facilitating smooth transactions. Two prominent methods often considered are Cash Against Documents (CAD) Payment Terms and the Letter of Credit (LC). While both serve to exchange goods for payment, they differ significantly in their mechanics, risk allocation, complexity, and suitability for various trade scenarios. Understanding these distinctions is vital for both importers and exporters to make informed decisions that align with their operational needs and risk tolerance, especially when navigating the nuances of international trade payment methods.

1. Risk Allocation: Buyer vs. Seller Perspective

The fundamental difference between CAD and LC lies in how they distribute risk between the buyer (importer) and the seller (exporter). With Cash Against Documents (CAD), the seller retains control over the goods until the buyer makes payment. In the typical Cash Against Documents procedure, the seller’s bank forwards shipping documents (like the bill of lading, commercial invoice, packing list, etc.) to the buyer’s bank. The buyer’s bank then releases these documents to the buyer only after payment has been received. From the seller’s perspective, this means they bear the risk that the buyer might not pay, leaving them with goods in a foreign port and incurring potential demurrage charges or the cost of rerouting. Conversely, the buyer faces minimal risk as they only pay once the documents proving shipment are presented, assuring them the goods are en route.

A Letter of Credit (LC), on the other hand, significantly shifts the risk from the seller to the issuing bank. An LC is a bank’s undertaking to pay the seller a specified sum of money, provided the seller presents conforming documents by a stipulated deadline. For the seller, an LC offers much greater security, as payment is guaranteed by a bank, irrespective of the buyer’s financial standing or willingness to pay. This mitigates the risk of non-payment almost entirely. The buyer, however, assumes the risk that they must pay if the documents conform to the LC terms, even if there are disputes regarding the quality or condition of the goods later on. The bank’s obligation is to the documents, not the underlying goods. This makes LCs a powerful tool for export payment terms for buyers, particularly when trust is low or transaction values are high.

2. Complexity and Cost Comparison

When comparing CAD vs Letter of Credit, their operational complexity and associated costs are critical factors. CAD is generally considered simpler and less expensive. The Cash Against Documents procedure involves fewer parties (typically the buyer, seller, and their respective banks acting as collection agents) and less stringent documentation requirements compared to an LC. The banking fees for CAD are usually limited to collection charges, which are modest. This simplicity makes CAD an attractive option for businesses looking to minimize administrative burden and transaction costs.

Conversely, Letters of Credit are significantly more complex and costly. An LC involves multiple parties, including the applicant (buyer), beneficiary (seller), issuing bank, and often an advising or confirming bank. The documentation required for an LC is exhaustive and must adhere strictly to the terms of the credit, which often refers to the Uniform Customs and Practice for Documentary Credits (UCP). Any discrepancies in the presented documents can lead to payment delays or refusal, requiring meticulous attention to detail. The banking fees for LCs are substantially higher, encompassing issuance fees, advising fees, confirmation fees (if applicable), and discrepancy fees. These costs can add a notable percentage to the total transaction value, making LCs more suitable for larger, high-value shipments where the added security justifies the expense and administrative effort.

3. When is CAD Preferable over LC for Export Payment Terms?

The choice between CAD and LC largely depends on the specific trade scenario, the relationship between the trading partners, and the level of risk tolerance. CAD is often preferred in situations where there is an established trust relationship between the buyer and seller, possibly after several successful transactions using other methods. It is also suitable for smaller transactions where the cost of an LC would be disproportionately high relative to the value of the goods. Exporters might consider CAD for buyers with whom they have a long-standing positive history, or in markets where political and economic stability is high, reducing the risk of payment default. For export payment terms for buyers, CAD offers a straightforward and cost-effective approach when the buyer’s creditworthiness is not a significant concern.

Conversely, an LC is almost always preferable, and often mandatory, when dealing with new trading partners, especially across different countries or cultures where trust is yet to be established. For high-value transactions, large volume shipments, or trade with regions prone to political or economic instability, an LC provides indispensable security to the seller. Furthermore, if the buyer’s creditworthiness is uncertain, or if the seller wishes to mitigate the risk of non-payment to the highest degree, the bank-guaranteed payment of an LC makes it the superior choice. Ultimately, the decision of CAD vs Letter of Credit hinges on a careful assessment of risk, cost, and the nature of the commercial relationship, ensuring that the chosen payment method supports secure and efficient international trade.

Benefits and Risks of Cash Against Documents Payment Terms

Cash Against Documents (CAD) payment terms represent a common and often preferred method in international trade, particularly when a degree of trust exists between the exporter and importer, or when the cost and complexity of a Letter of Credit (L/C) are deemed unnecessary. As a crucial component of export payment terms for buyers, CAD strikes a balance between the buyer’s need for security and the seller’s desire for timely payment. In this setup, the seller typically ships the goods and then presents the shipping documents (such as the bill of lading, commercial invoice, and packing list) to their bank. This bank, acting as the remitting bank, forwards these documents to the importer’s bank (the collecting bank). The collecting bank then releases the documents to the importer only upon payment (Documents Against Payment, D/P) or acceptance of a bill of exchange (Documents Against Acceptance, D/A). Understanding the benefits and risks associated with CAD is vital for businesses engaging in global commerce.

1. Advantages for Exporters (Sellers)

For exporters, CAD offers several appealing advantages over open account terms. Firstly, it provides a stronger assurance of payment, as the exporter’s bank retains control of vital shipping documents until the importer fulfills their payment obligation or accepts the bill of exchange. This significantly reduces the risk of non-payment compared to open account sales, offering the seller more security without the stringent requirements and costs of an L/C. Secondly, the Cash Against Documents procedure is generally simpler and less bureaucratic than an L/C, leading to lower banking fees and faster processing. Exporters can receive payment relatively quickly once documents are accepted or paid, improving their cash flow. Moreover, it fosters trust and potentially stronger, long-term business relationships, while allowing the exporter to retain leverage through document control until payment.

2. Advantages for Importers (Buyers)

From an importer’s perspective, CAD offers substantial benefits, particularly concerning cash flow management and risk mitigation compared to upfront payments or the complexities of an L/C. Unlike advance payment, where the buyer assumes all risk by paying before shipment, CAD ensures the buyer does not part with funds until goods have been shipped and relevant documents are available. This means the importer retains control over capital for longer, improving liquidity. Furthermore, the importer gets the opportunity to examine shipping documents before making payment or accepting the bill of exchange. This allows them to verify document compliance with the sales contract, ensuring correct goods have been dispatched and are en route. This pre-payment document verification is a critical safeguard. Additionally, CAD terms are typically less expensive than an L/C for the buyer, incurring fewer bank charges and administrative costs. This makes CAD an attractive and cost-effective international trade payment method for buyers, especially those with established supplier relationships.

3. Navigating the Risks Associated with CAD

Despite its advantages, CAD carries risks for both exporters and importers. For exporters, the primary risk is the importer’s potential refusal to pay or accept documents upon arrival. If the importer defaults, goods may be stranded at the destination port, incurring significant demurrage and storage charges. The exporter would then need to find an alternative buyer or arrange for return, both costly propositions. Importer payment delays also impact exporter cash flow.

For importers, while document inspection is a benefit, it doesn’t guarantee the quality or quantity of physical goods. Documents can be compliant, yet the actual cargo might be damaged, incorrect, or even missing upon arrival. This leaves the buyer in a precarious position, having paid for documents representing unsatisfactory goods. Recourse can be challenging and expensive, often requiring legal action in a foreign jurisdiction. There’s also the risk of the exporter shipping non-conforming goods or even fraudulent documents, making diligent verification crucial.

To mitigate these risks, both parties should undertake due diligence. Exporters should vet buyers thoroughly, checking creditworthiness. Importers should consider pre-shipment inspections by independent third parties for high-value goods to ensure cargo matches specifications before shipment. Both parties should use reputable banks and ensure all contractual terms are clear. Trade credit insurance can also offer a safety net for exporters. In situations where trust is insufficient or transaction value is exceptionally high, reverting to more secure methods like an L/C or seeking advice on alternative international trade payment methods may be prudent. Understanding these dynamics is key to leveraging Cash Against Documents Payment Terms effectively in global trade.

Best Practices for Using Cash Against Documents in 2025

Cash Against Documents (CAD) continues to be a widely adopted and cost-effective payment method in international trade, striking a balance between the open account’s trust and the Letter of Credit’s security. In 2025’s dynamic global landscape, mastering its intricacies is crucial for businesses looking to optimize their cross-border transactions. While less secure for the exporter than a Letter of Credit, CAD offers advantages in terms of cost and speed, making it an attractive option for established trading partners or when the risk is deemed acceptable. Understanding the nuances of “Cash Against Documents Payment Terms” is vital for both importers and exporters aiming for smooth, compliant, and efficient trade operations. This section will delve into practical advice, legal considerations, and strategic tips to navigate the complexities of CAD in the modern era.

1. Ensuring Clear Contractual Agreements and Documentation

The bedrock of any successful Cash Against Documents transaction lies in the precision and clarity of its underlying contractual agreements and the integrity of the accompanying documentation. Before initiating any shipment, both parties – exporter and importer – must agree upon and meticulously define all terms. This includes the goods’ specifications, price, delivery schedule, “Cash Against Documents Payment Terms,” and, crucially, the exact documents required for payment release. Standard documents typically include the commercial invoice, packing list, bill of lading (or air waybill), and certificate of origin. Depending on the nature of the goods or regulatory requirements, additional documents such as inspection certificates, insurance policies, or health certificates might be necessary. Any discrepancy, however minor, between the documents presented and those specified in the collection instructions can lead to delays, demurrage charges, or even payment refusal. Businesses should employ robust internal processes for document generation and verification, ensuring that all details align perfectly with the sales contract. This proactive approach minimizes risks and streamlines the entire “Cash Against Documents procedure”, reducing potential disputes and fostering trust between trading partners. For more insights into international trade payment terms, explore the resources on Cash Against Documents Payment Terms.

2. The Role of Reliable Banks and Intermediaries

In a Cash Against Documents arrangement, banks act as crucial intermediaries, facilitating the exchange of documents for payment but without undertaking any payment obligation themselves, unlike in a Letter of Credit. The exporter’s bank (remitting bank) sends the collection documents to the importer’s bank (collecting bank), which then releases these documents to the importer upon payment or acceptance of a draft. The reliability and efficiency of these banking partners are paramount. Exporters should select a remitting bank with strong international correspondent banking relationships, particularly in the importer’s country, to ensure swift and secure document handling. Importers, similarly, benefit from using a collecting bank known for its expertise in international trade finance and its diligent handling of collection instructions. Clear communication between both banks is essential, as is their adherence to the Uniform Rules for Collections (URC 522), published by the International Chamber of Commerce (ICC), which govern most international collections. While CAD offers less security than a “CAD vs Letter of Credit” scenario, a robust banking network mitigates operational risks. Understanding the full scope of “International trade payment methods” involves recognizing the critical support provided by well-chosen financial institutions.

3. Adapting to Global Trade Dynamics and Regulations

The global trade environment in 2025 is characterized by evolving geopolitical landscapes, technological advancements, and a growing emphasis on regulatory compliance. Businesses utilizing Cash Against Documents must remain agile and informed. This involves conducting thorough due diligence on both trading partners and destination countries. Sanctions regimes, anti-money laundering (AML) regulations, and specific import/export controls can change rapidly, impacting the feasibility and legality of transactions. Staying abreast of these changes is not merely good practice but a legal necessity to avoid severe penalties. Furthermore, logistical considerations, such as potential supply chain disruptions or changes in shipping routes, can affect document presentation timelines and impact the successful execution of “Export payment terms for buyers”. Leveraging digital platforms for document exchange, where permissible and secure, can enhance speed and reduce errors. Companies should also consider obtaining trade credit insurance for their CAD transactions, offering an added layer of protection against buyer default, especially when dealing with new or less familiar partners. For further reading on navigating international trade, an excellent resource on various payment methods and their implications can be found at the International Chamber of Commerce (ICC) website: ICC Incoterms and Rules for Collections. Proactive risk assessment and continuous adaptation to these dynamics are key to leveraging “Cash Against Documents Payment Terms” effectively and securely in today’s interconnected world. For more details on efficient payment options, visit vietnamsuppliers.com for Cash Against Documents Payment Terms. Additionally, a comprehensive guide to understanding Cash Against Documents Payment Terms is available. And finally, for streamlined international transactions, consider the benefits of Cash Against Documents Payment Terms.

Partner with Vietnam’s Leading Suppliers

Looking for reliable suppliers in Vietnam? Contact VietnamSuppliers.com today to connect with verified manufacturers and exporters across all industries.

—————————————

References

– Payment Methods: https://www.trade.gov/payment-methods

– ICC Uniform Rules for Collection (URC 522): https://www.iccwbo.org/publication/uniform-rules-for-collection-urc-522/

– Uniform Customs and Practice for Documentary Credits (UCP): https://www.investopedia.com/terms/u/ucp.asp

– international trade payment method: https://www.investopedia.com/terms/i/international-trade-payment-methods.asp

– ICC Incoterms and Rules for Collections: https://iccwbo.org/resources-for-business/incoterms-rules/